Weekly macroeconomic and market update 14 December 2015

Weekly macroeconomic and market update

Macro headlines

There were fresh signs of market stress last week, fueling a sense of unease amongst skittish investors.Brentcrudeoil slipped below US$38 per barrel to a seven-year low amid high inventory levels and a report that actual OPEC production had increased to 31.7 million barrels per day compared to a target of 30 million. At the end of last week we also saw the failure of a major distressed debt fund (Third Avenue Management) with over US$700 million, and rumours began to circulate that a US$400 million credit hedge fund might also be in trouble. Whilst these funds are very much at the periphery, it has served to highlight some of the tensions around the edges of markets, and has not been helping sentiment.

There was plenty of excitement to come out of China last week, with a sharp fall of US$87 billion in the level of foreign exchange reserves, and the authorities laying the groundwork for fresh depreciation of the currency. Despite this fall, the official reserves still stood at US$3.43 trillion in value at the end of November, and according to reports the US$87 billion drop equates to roughly US$57 billion of actual sales by the Peoples’ Bank of China (the remaining US$30 billion is accounted for by the foreign exchange market effects for non-US dollar holdings). Given that the trade surplus for November was US$54.1 billion, that suggests another month of capital outflows more than US$100 billion, as we witnessed at points over the summer when investors in China had a clear imperative to get their capital out. Fears over the potential for fresh currency devaluation appear to have been well-founded: at the end of the week the Peoples’ Bank of China announced it would look to measure the value of the Renminbi against a basket of currencies instead of just the US dollar. Given the dramatic strengthening of the US dollar, and therefore the Renminbi, against other major currencies, this change would clearly give them scope to allow the Renminbi to devalue against a strong US dollar whilst making it hard for others to level accusations of ‘unfair’ currency manipulations, particularly from the US. As we’ve said previously, given the Renminbi already appears over-valued when measured against a broader basket of currencies, and as the US appears set to embark on a new interest rate cycle, this could well be the prelude to a fresh bout of currency depreciation.

The final reading for Japanese third quarter GDP was dramatically revised up from a -0.8% annualised fall to a +1.0% annualised gain. The revision means that Japan hasn’t been in a recession, and brings back into question the reliability of the authority’s estimate methodology. The revision comes as a number of other economic indicators have also been suggesting a more positive outlook. Recent surveys of both the current economic condition and the near-term outlook suggested there was broad optimism in the wider economy (initial Concident Index reading of 114.3 in October from 112.3 in September, The Leading Economic Index was at 102.9 from 101.6). Machinery orders were also supportive, accelerating to 10.7% month-on-month growth for October, from 7.5% the month before and comfortably ahead of expectations for a contraction. It wasn’t all roses though, with some notes of caution evident in the outlook of large manufacturing, where the BSI Large Manufacturing Index slipped from 11 to 3.8. The Economy Watchers surveys, which polls the mood as gauged from those servicing consumers directly, such as cab drivers, slipped on both the current conditions and outlook, with readings of 46.1 and 48.2 respectively, indicating continued pessimism.

Other macro events

Markets

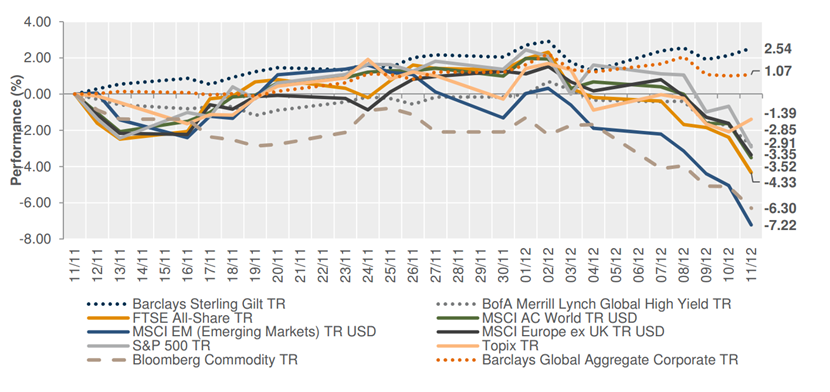

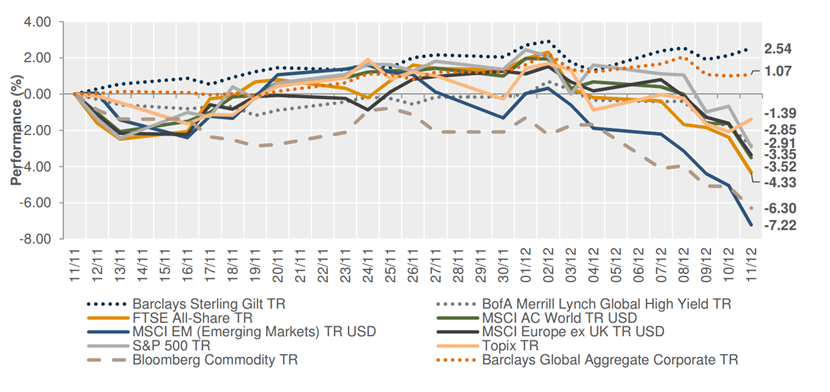

Negative sentiment hit markets pretty hard last week, sending equities lower with investors heading into the perceived safe arms of sovereign bonds.

1 MONTH PERFORMANCE OF MAJOR ASSET CLASSES

Week ahead

Arguably the most important macroeconomic event of the year on Wednesday we are expecting the US Federal Reserve to finally increase interest rates for the first time in almost a decade. Markets are generally expecting a standard 25 bps hike to 0.5%, although there remains plenty of scope for surprise and disappointment. Aside from any variation in the actual hike (would they risk a half-hike of 10-15 bps or could they even delay at this juncture?), the statement and press conference will be crucial for market sentiment, with any excessively dovish or hawkish overtones likely to elicit a strong market reaction.

Monday: The Eurozonereports on industrial production, with growth expected to have accelerated from 1.3% to 1.7%

Tuesday: UK inflation in the morning is forecast to have increased 0.2% to just about positive at 0.1% year on year. Later in the morning is the ZEW economic surveys from Germany and in the afternoon US inflation is reported, expected at 0.5% year on year at a headline rate, with core inflation at 2.0%.

Wednesday: Notthatanyone is likely to be looking at anything else, but aside from the FOMC result, flash Manufacturing and Services PMI in the Eurzone are expected to remain stable in the early-to-mid 50s. UK earnings and unemployment will also be reported. Along with the US FOMC interest rate decision, we will also have fresh FOMC projections and some supporting mid-level economic data.

Thursday: As markets digest the FOMC output, German Ifo business survey data are released, together with UK retail sales.In the afternoon, US leading index and initial jobless numbers are updated.

Friday: A quiet end to an important week is expected. Overnight Chinese house price data are released, along with the Bank of Japan’s interest rate decision. In the afternoon, US Flash Services and Composite PMI from Market see us out.

This article was previously published on Tilney prior to the launch of Evelyn Partners.

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.